Montgomery County Planning Commission

Montgomery County Planning Commission

Beth Ann Rosica: A tale of two districts – same school district audit yields two very different responses

Twelve school districts across the commonwealth were audited, resulting in similar findings. And while no illegal activities were discovered, Pennsylvania’s auditor general raised a number of concerns and recommendations for school boards to improve their stewardship of tax dollars on behalf of taxpayers.

(How districts manipulated their budgets, moved money around between funds, and requested exceptions from the state to raise taxes without taxpayer input are explained in this recent article.)

Neshaminy School District in Bucks County and North Penn School District in Montgomery County were both included in the audit. While the findings were nearly identical for both districts, the two districts’ responses to the audit were very different. Perhaps this is related to the composition of their school boards? In North Penn, Democrats hold all nine seats while Neshaminy has a more balanced board with five Democrats and four Republicans.

The findings for both districts related to requesting referendum exceptions to raise taxes without taxpayer input by manipulating budgets and transferring funds to different accounts. Page 96 of the audit details Neshaminy’s findings: “Neshaminy routinely requests referendum exceptions despite having sufficient funding for anticipated annual expenditures. Neshaminy designates its General Fund as commitments and assignments to increase taxes while retaining millions of dollars not used timely for designated purposes.”

The report further stated that some of the practices were enacted under the former chief financial officer. “When questioned Neshaminy’s Chief Financial Officer (CFO) stated that the district’s former CFO routinely applied for referendum exceptions as a budget tool to keep the option of increasing taxes above the index available until the end of the budget process each year.” (page 96)

The Neshaminy superintendent, Dr. Rob McGee, agreed with the audit recommendations as stated in his November 28, 2022, email to the auditor general’s office. “We are in receipt of the draft report, agree with each finding and plan to comply with all recommendations (given board approval).” (page 100)

While the district did not respond to a request for a comment, the board’s actions following the release of the audit are consistent with the superintendent’s statement that they were in agreement with the findings and recommendations. Recommendation #2 (page 99) encouraged the board to pass a resolution to not increase taxes above the district’s index when there are existing funds available to cover expenses in the General Fund. On January 25, 2023, the Neshaminy board members passed and signed the resolution that the auditor general recommended.

Overall, Neshaminy’s response to the auditor general was positive, and subsequently, the board enacted at least one of the recommendations.

Conversely, North Penn school district had almost identical findings, yet reacted quite differently. Page 112 identifies the findings. “North Penn routinely requests referendum exceptions despite having sufficient funding for anticipated annual expenditures. North Penn increased taxes despite having unused committed funds and while transferring millions of dollars each year.”

It appears that the district administration did not dispute the concerns during the audit process. The North Penn CFO acknowledged that applying for referendum exceptions is a standard practice, used as a budgetary tool for flexibility. Furthermore, “the CFO acknowledged that the commitment of $16.8 million was not spent or needed during the three FYE June 30, 2019, 2020, and 2021.” (page 113)

The report stated that the board placed an unnecessary excess burden on taxpayers over multiple years. “This excess tax burden was compounded in future years because the Board did not reverse the unneeded tax increase.” (page 113)

The audit contained five similar recommendations to the Neshaminy recommendations, including “North Penn’s policy allows it to increase taxes while retaining millions of dollars of unspent funds for several years. The Board should reconsider its policies and practices to help lessen the tax burden on its taxpayers as a matter of prudent stewardship.” (page 115)

The superintendent’s response to the audit on page 117 states that the district would take all five recommendations under advisement, albeit with some pushback on the first two recommendations. However, in a public statement released after the audit, there was no mention of considering the recommendations, and instead a defensive response. “I am disappointed to hear the misleading rhetoric regarding this report.”

The superintendent further defended the district’s actions by reminding residents that their tax rate is the fifth lowest in Montgomery County and that the district has received financial awards and a high Moody’s rating.

A request for comment from the district was answered with the same prepared statement.

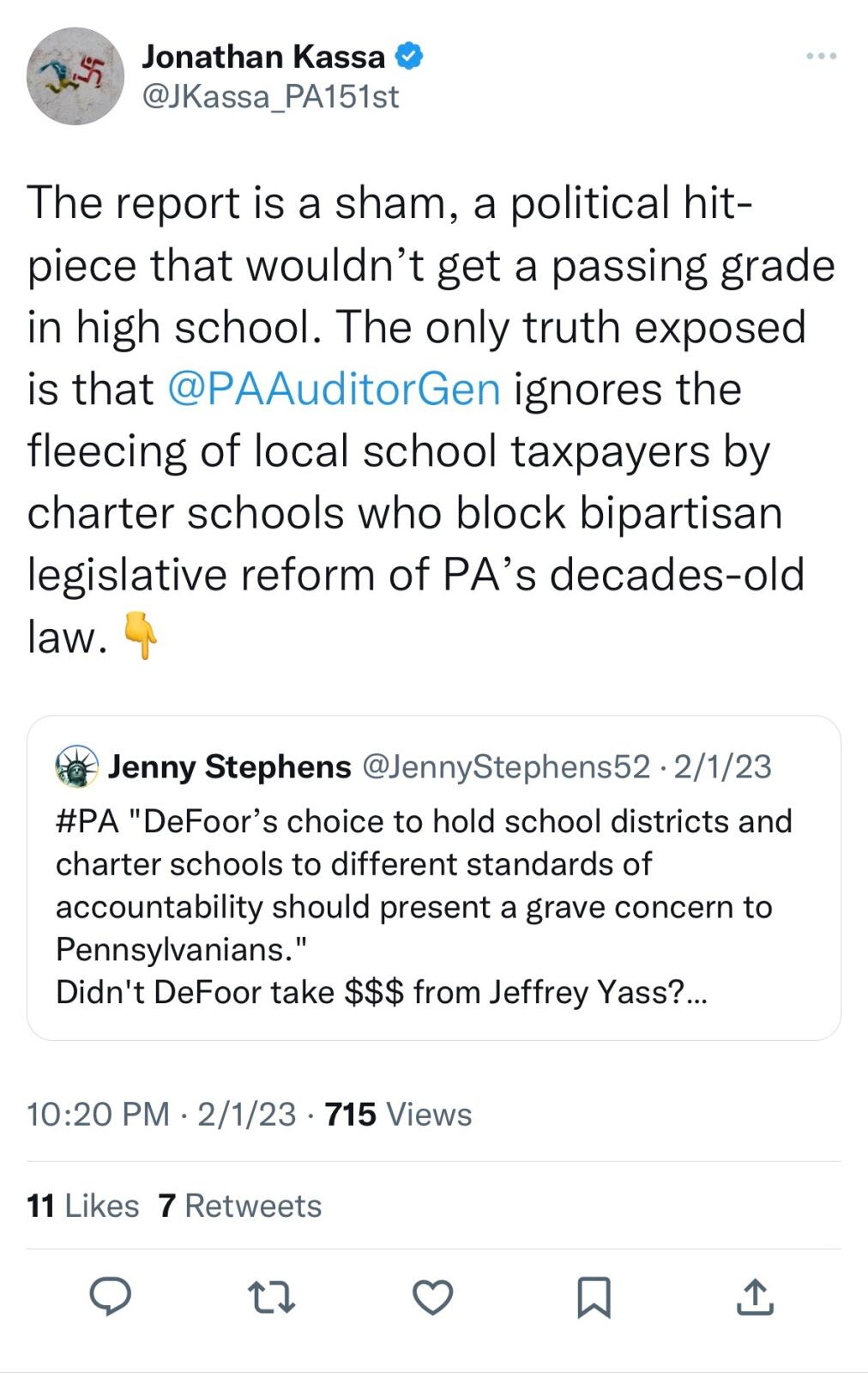

Additionally, both the district CFO, Steve Skrocki, and a school board member, Jonathan Kassa, voiced their vehement opposition to the audit and its findings on their social media accounts.

While there was no report of illegal activity for either district, both districts were cited for lack of transparency to taxpayers through a manipulation of the budgets. Neshaminy agreed with the findings and has already enacted at least one of the recommendations. North Penn and their 9-0 Democratic board chose not only to ignore their commitment to take the recommendations under advisement, but both a district administrator and at least one board member posted publicly about their dissatisfaction with the audit and its findings. (see below) They referred to the audit as “clumsy”, and a “sham, political hit piece.”

Neshaminy and its board should be lauded as an example of transparency and commitment to its taxpayers, while North Penn should be questioned about why they changed their initial response to the audit and then used social media to undermine the audit process. The North Penn school board has five seats up for election this year, and ultimately the taxpayers will decide whether they are pleased with the district and board’s response to the audit.

Beth Ann Rosica resides in West Chester, has a Ph.D. in Education, and has dedicated her career advocating on behalf of at-risk children and families.

In the final post shown in the article, the writer alludes to different standards for school districts and charters. Two things should be noted for the readers. First, charter schools have no taxing authority. The reimbursement received is based on a Commonwealth of PA formula and flows through the school district where the charter school is located. It is based on a capitation model using average daily attendance for the amount that goes to the charter school, so it can fluctuate on a monthly basis. Second, charter schools are required to undergo an independent audit on an annual basis and those audit findings sent into the Department of Education and be available for public review.